Student loan forgiveness is a program that cancels all or part of a borrower’s education debt. Under certain circumstances, the borrower may not be required to repay some or all of their loans. There are several student loan forgiveness programs available, each with its own specific requirements and eligibility criteria. Some programs are open to all borrowers, while others are only available to certain types of borrowers, such as teachers or public service workers. Some common types of student loan forgiveness programs include:

- Public Service Loan Forgiveness (PSLF): This program is available to borrowers who work in certain public service jobs and make 120 qualifying monthly payments on their Direct Loans. After completing the required payments, the remaining balance on the borrower’s Direct Loans will be forgiven.

- Teacher Loan Forgiveness: This program is available to teachers who teach full-time for five complete and consecutive academic years in certain low-income schools or educational service agencies. Eligible teachers may be able to receive forgiveness on Direct Subsidized and Unsubsidized Loans, as well as Subsidized and Unsubsidized Federal Stafford Loans.

- Perkins Loan Cancellation and Discharge: This program is available to borrowers who are employed in certain professions, such as teaching, nursing, or law enforcement. Borrowers may be able to have a portion of their Perkins Loans forgiven if they meet certain employment and repayment requirements.

Student loans can be a valuable investment in your future, but they can also become a burden if not carefully considered or misused. If you have a student loan or are considering getting one, it’s important to determine if you may be eligible for student loan forgiveness. Our estimates suggest that at least half of student loan borrowers may qualify to have all or part of their loan canceled through a process called Student Loan Forgiveness. To be eligible, you may need to perform volunteer work, serve in the military, practice medicine in certain communities, or meet other requirements.

There are many other student loan forgiveness programs available, and the specific requirements and eligibility criteria can vary. It’s important for borrowers to carefully review the terms and conditions of any forgiveness program before applying.

US Govt Student Loan Forgiveness Proposal

President Biden’s proposal to forgive up to $20,000 in student loans is currently on hold due to court orders. The Supreme Court is scheduled to hear arguments on this loan forgiveness plan in February 2023.

On August 24, 2022, President Biden announced plans to forgive up to $20,000 in student loan debt for eligible borrowers. Although the specifics of the program are not yet finalized (and it may face legal challenges due to the possibility of being implemented through executive order), here is what is currently known:

- Pell Grant recipients with loans held by the Department of Education (usually Direct student loans and certain federally-held FFEL and Perkins Loans) may receive $20,000 in debt cancellation.

- Non-Pell Grant recipients may receive $10,000 in debt cancellation.

To be eligible, you must have an adjusted gross income (AGI) of less than $125,000 for individuals or $250,000 for married couples and head-of-household.

Please note that the maximum amount of forgiveness cannot exceed your current loan balance. For example, if you only have a $9,000 balance, that would be the maximum amount of forgiveness you could receive. If you made voluntary payments on your student loans during the Covid-19 payment pause, you may request a refund of those payments.

It appears that there will be a cutoff for loans made before June 30, 2022, and a consolidation cutoff date of September 29, 2022. This means that current college students (not just incoming Freshmen, but other years) may be eligible for loan forgiveness even if they have not yet graduated.

While some borrowers may have this forgiveness applied automatically, others will need to apply for it (and potentially verify their income). You can typically fill out the One-Time Student Loan Forgiveness Application online, but it has been temporarily removed due to ongoing legal challenges to the legality of President Biden’s student loan forgiveness plan.

Repayment Plan Based Student Loan Forgiveness:

Student loan forgiveness plans allow borrowers to have any remaining balance on their loans forgiven at the end of their repayment term, as long as they are enrolled in a qualifying repayment plan. Keep in mind that these plans have certain eligibility requirements and that loan forgiveness is generally considered taxable income. However, President Biden has made student loan forgiveness and discharge tax-free for Federally-held loans until the end of 2025. To apply for a repayment plan with student loan forgiveness, contact your lender or visit StudentLoans.gov. It’s worth noting that if you have no remaining balance at the end of your loan term, you will not be eligible for forgiveness.

Income-Based Repayment (IBR)

Income-Based Repayment (IBR) is a repayment plan for federal student loans that caps your monthly payments at a percentage of your income. Your payment amount is based on your adjusted gross income, family size, and the amount of your eligible student loans. IBR is designed to make your monthly student loan payments more affordable by basing them on your income. If you have high levels of student loan debt relative to your income, IBR could potentially lower your monthly payments.

To be eligible for IBR, you must have a partial financial hardship, which means that the monthly amount you would be required to pay on your eligible student loans under a standard repayment plan is higher than the monthly amount you would be required to pay under IBR. If you have no financial hardship, you will not be able to enroll in IBR.

If you enroll in IBR and make payments for 25 years (or 20 years if you work in a public service job), any remaining balance on your student loans will be forgiven. However, it’s important to note that the forgiven amount may be considered taxable income by the IRS, unless you are eligible for an exception or exclusion.

Pay As You Earn (PAYE)

Pay As You Earn (PAYE) is a repayment plan for federal student loans that caps your monthly payments at a percentage of your income. Your payment amount is based on your adjusted gross income, family size, and the amount of your eligible student loans. PAYE is designed to make your monthly student loan payments more affordable by basing them on your income. If you have high levels of student loan debt relative to your income, PAYE could potentially lower your monthly payments.

To be eligible for PAYE, you must have a partial financial hardship, which means that the monthly amount you would be required to pay on your eligible student loans under a standard repayment plan is higher than the monthly amount you would be required to pay under PAYE. If you have no financial hardship, you will not be able to enroll in PAYE.

If you enroll in PAYE and make payments for 20 years (or 25 years if you work in a public service job), any remaining balance on your student loans will be forgiven. However, it’s important to note that the forgiven amount may be considered taxable income by the IRS, unless you are eligible for an exception or exclusion.

The Pay As You Earn Repayment Plan (PAYE) is similar to the Income-Based Repayment Plan (IBR) in that it caps your monthly payments at a percentage of your income and forgives any remaining balance after a certain number of years. Specifically, with PAYE, you will not pay more than 10% of your discretionary income, and your loan will be forgiven after 20 years (or 25 years if you work in a public service job).

One key difference between PAYE and IBR is that only certain loans taken out after 2007 are eligible for PAYE. If you have older loans, you may not be able to enroll in this repayment plan. It’s worth noting that, like IBR, the forgiven amount under PAYE may be considered taxable income by the IRS unless you are eligible for an exception or exclusion.

Revised Pay As You Earn (RePAYE)

Revised Pay As You Earn (RePAYE) is a repayment plan for federal student loans that caps your monthly payments at a percentage of your income. Your payment amount is based on your adjusted gross income, family size, and the amount of your eligible student loans. RePAYE is designed to make your monthly student loan payments more affordable by basing them on your income. If you have high levels of student loan debt relative to your income, RePAYE could potentially lower your monthly payments.

Unlike the Pay As You Earn (PAYE) repayment plan, RePAYE is available to borrowers with any type of federal student loan, regardless of when the loan was taken out. To be eligible for RePAYE, you must have a partial financial hardship, which means that the monthly amount you would be required to pay on your eligible student loans under a standard repayment plan is higher than the monthly amount you would be required to pay under RePAYE. If you have no financial hardship, you will not be able to enroll in RePAYE.

If you enroll in RePAYE and make payments for 20 years (or 25 years if you work in a public service job), any remaining balance on your student loans will be forgiven. However, it’s important to note that the forgiven amount may be considered taxable income by the IRS, unless you are eligible for an exception or exclusion.

Revised Pay As You Earn (RePAYE) is a repayment plan for federal student loans that is similar to Pay As You Earn (PAYE), but it is available to borrowers with any type of federal student loan, regardless of when the loan was taken out. RePAYE became available on December 17, 2015, and it caps your monthly payments at 10% of your discretionary income. Your loan will be forgiven after 20 years (or 25 years if you work in a public service job).

The RePAYE plan includes an interest subsidy that helps cover 50% of the interest in cases where the new payments cannot keep up with the accruing interest. This can be helpful for borrowers who have high levels of student loan debt relative to their income and may not be able to afford their monthly payments under a standard repayment plan.

It’s worth noting that, like PAYE, the forgiven amount under RePAYE may be considered taxable income by the IRS unless you are eligible for an exception or exclusion.

Income Contingent Repayment (ICR)

The Income Contingent Repayment Plan (ICR) is a repayment plan for federal student loans that does not have initial income requirements like the Income-Based Repayment (IBR) or Pay As You Earn (PAYE) plans. This means that any borrower who has eligible loans can enroll in ICR. Under this plan, your monthly payments will be the lesser of the following:

- 20% of your discretionary income

- The amount you would pay on a repayment plan with a fixed payment over the course of 12 years, adjusted according to your income

In other words, your monthly payments under ICR will be based on your income, but they may also be higher than they would be under IBR or PAYE if your income is higher. It’s worth noting that, like IBR and PAYE, the forgiven amount under ICR may be considered taxable income by the IRS unless you are eligible for an exception or exclusion.ICR plan, your loans will be forgiven at the end of 25 years.

Career-Based Student Loan Forgiveness Options:

There are various student loan forgiveness options available to borrowers depending on their career paths. One of the most popular options is Public Service Loan Forgiveness, which offers a significant amount of forgiveness in a relatively short period of time and is tax-free. It is also available to a wide range of jobs in the public service sector. However, it’s worth noting that Public Service Loan Forgiveness is not the only career-based student loan forgiveness option available.

Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness Program offers student loan forgiveness on qualifying loans after you have made 120 payments (over a period of 10 years). This is a popular option for borrowers who are looking for student loan forgiveness and are eligible for it.

Public service employment, as defined by the program, includes any employment with a federal, state, or local government agency, entity, or organization or a tax-exempt not-for-profit organization under Section 501(c)(3) of the Internal Revenue Code. The specific nature of the job does not matter for the purposes of Public Service Loan Forgiveness. Some examples of jobs that may qualify for the program include government workers, military personnel, teachers, public health professionals, and workers in the public interest law sector. However, the organization must not be a labor union or a partisan political organization.

For example:

- Government Workers (Federal, State, Local).

- Emergency management.

- Military service.

- Public safety or law enforcement services.

- Public health services.

- Teachers.

- Public education or public library services.

- School library and other school-based services.

- Public interest law services.

- Early childhood education.

- Public service for individuals with disabilities and the elderly.

Temporary Expanded PSLF (TEPSLF)

Temporary Expanded Public Service Loan Forgiveness (TEPSLF) is a temporary program that was established to give certain borrowers who were denied forgiveness under the Public Service Loan Forgiveness (PSLF) program a second chance to have their loans forgiven. To be eligible for TEPSLF, you must:

- Have made at least one payment under an income-driven repayment plan

- Have at least one Direct Loan that is not in default

- Have not received a forgiveness benefit under PSLF or any other loan forgiveness program

- Have made at least 120 payments on your Direct Loans under an income-driven repayment plan or a repayment plan that is based on your income, as well as under the standard repayment plan (or an equivalent repayment plan)

If you meet these criteria and your employer is a government or not-for-profit organization that qualifies for PSLF, you may be eligible for TEPSLF. However, it’s important to note that this is a temporary program that is set to expire on September 30, 2027, and it is only available to a limited number of borrowers. If you think you may be eligible for TEPSLF, you should contact your loan servicer to learn more.

Attorney Student Loan Forgiveness Program:

The Attorney Student Loan Forgiveness Program is a student loan forgiveness program that is specifically designed for attorneys who work in government or non-profit organizations. To be eligible for the program, you must:

- Have an outstanding balance on your student loans

- Be an attorney who is employed full-time by a government or non-profit organization

- Have made at least 120 payments on your student loans while working for a qualifying employer

If you meet these criteria, you may be eligible for student loan forgiveness under the Attorney Student Loan Forgiveness Program. The amount of forgiveness you can receive depends on the type of work you do and the amount of your student loan debt. For example, attorneys who work in public interest law may be eligible for a higher level of forgiveness than those who work in other areas.

It’s worth noting that the Attorney Student Loan Forgiveness Program is separate from the Public Service Loan Forgiveness (PSLF) program, which is also available to attorneys who work in government or non-profit organizations. To learn more about the Attorney Student Loan Forgiveness Program and to see if you are eligible, you should contact your loan servicer.

Faculty Loan Repayment Program

The Faculty Loan Repayment Program from the Health Resource and Services Administration (HRSA) offers student loan repayment assistance to help recruit and retain health professions faculty members. This program encourages students to pursue careers as faculty members in the health care field, which is important for training and supporting the next generation of educators.

Under the Faculty Loan Repayment Program, you may be eligible to receive up to $40,000 in student loan repayment, as well as additional money to offset the tax burden of the program. If you are interested in applying for this program and you meet the eligibility requirements, you should contact HRSA to learn more.

Federal Employee Student Loan Repayment Program

The Federal Employee Student Loan Repayment Program is a student loan repayment benefit that is available to federal employees who are working in certain occupations or agencies. Under this program, the federal government will repay a portion of your student loans on your behalf if you meet the eligibility requirements.

To be eligible for the Federal Employee Student Loan Repayment Program, you must:

- Be a federal employee who is working in a position that is eligible for the program

- Have a qualifying student loan that is in repayment

- Meet any other requirements that may be specific to your agency or occupation

The amount of student loan repayment you can receive under the Federal Employee Student Loan Repayment Program depends on your agency’s funding and the specific terms of the program. Some agencies may offer up to $10,000 per year in student loan repayment, up to a maximum of $60,000 over the course of your career.

If you are interested in applying for the Federal Employee Student Loan Repayment Program, you should contact your human resources office or visit the Office of Personnel Management’s website to learn more.

John R. Justice Student Loan Repayment Program

The John R. Justice Student Loan Repayment Program is a student loan repayment program that is specifically designed for state and federal public defenders and state prosecutors. The program is named after John R. Justice, a former South Carolina Attorney General and Supreme Court Justice.

Under the John R. Justice Student Loan Repayment Program, state and federal public defenders and state prosecutors may be eligible to receive student loan repayment assistance if they meet the following requirements:

- Are employed full-time as a state or federal public defender or state prosecutor

- Have an outstanding balance on their student loans

- Have made at least 120 payments on their student loans

If you meet these eligibility requirements and you are interested in applying for the John R. Justice Student Loan Repayment Program, you should contact your state or federal agency to learn more. The amount of student loan repayment you can receive under this program depends on the specific terms of the program and the amount of your student loan debt.

National Health Service Corps

The National Health Service Corps (NHSC) is a program that offers loan repayment and scholarship opportunities to primary care medical, dental, and behavioral health providers who work in underserved areas of the United States. The NHSC was created to help address shortages of primary care providers in underserved areas and to encourage more healthcare professionals to work in these areas.

To be eligible for the NHSC loan repayment program, you must:

- Be a U.S. citizen or national

- Be a licensed primary care medical, dental, or behavioral health provider

- Have an outstanding balance on your student loans

- Be employed at an NHSC-approved site in an underserved area

If you meet these eligibility requirements and you are interested in applying for the NHSC loan repayment program, you should visit the NHSC’s website to learn more and to submit an application. The amount of loan repayment you can receive under this program depends on the specific terms of the program and the amount of your student loan debt.

National Institutes of Health (NIH) Loan Forgiveness

The National Institutes of Health (NIH) offers five extramural Loan Repayment Programs (LRPs) for researchers who are working in specific fields. These LRPs include the Clinical Research LRP, the Pediatric Research LRP, the Contraception & Infertility Research LRP, the Health Disparities Research LRP, and the Clinical Research LRP for Individuals from Disadvantaged Backgrounds.

In exchange for student loan repayment assistance under these LRPs, awardees are required to fulfill a service obligation by conducting qualifying research supported by a domestic nonprofit or U.S. government (Federal, state, or local) entity for 50% of their time (at least 20 hours per week based on a 40-hour week) for two years. The NIH makes quarterly student loan repayments to awardees as they fulfill their service obligation. If you are interested in applying for one of the NIH’s Loan Repayment Programs, you should visit the NIH’s website to learn more and to submit an application.

The National Institutes of Health (NIH) will repay a portion of your student loan debt through its Loan Repayment Programs (LRPs). The amount of repayment you can receive is based on the amount of your eligible education debt at the start of your LRP contract. Under these programs, the NIH will pay 25% of your eligible education debt each year, up to a maximum of $35,000 per year. If you are interested in applying for one of the NIH’s Loan Repayment Programs, you should visit the NIH’s website to learn more and to submit an application.

NURSE Corps Loan Program

The Nurse Corps Repayment Program is a student loan repayment program that is designed to support registered nurses (RNs), advanced practice registered nurses (APRNs), and nurse faculty. Under this program, you may be eligible to receive student loan repayment assistance if you meet the following criteria:

- You are a RN, APRN, or nurse faculty member who has attended an accredited school of nursing

- You are employed at an eligible Critical Shortage Facility in a high need area (for RNs and APRNs)

- You agree to fulfill a two-year work commitment at the facility

If you meet these eligibility requirements, you may be eligible to receive student loan repayment assistance of up to 85% of your unpaid nursing education debt. To learn more about the Nurse Corps Repayment Program and to see if you are eligible, you should visit the Health Resources and Services Administration’s website.

SEMA Loan Forgiveness Program

The SEMA Loan Forgiveness Program is a student loan forgiveness program that is specifically designed for individuals who are working in the motor vehicle industry. The program is administered by the Specialty Equipment Market Association (SEMA) and is funded by the U.S. Department of Education.

To be eligible for the SEMA Loan Forgiveness Program, you must:

- Be a U.S. citizen or national

- Be employed in the motor vehicle industry

- Have an outstanding balance on your student loans

- Meet any other requirements that may be specific to the program

If you meet these eligibility requirements and you are interested in applying for the SEMA Loan Forgiveness Program, you should visit the SEMA’s website to learn more and to submit an application. The amount of student loan forgiveness you can receive under this program depends on the specific terms of the program and the amount of your student loan debt.

Teacher Loan Forgiveness Program

The Teacher Loan Forgiveness Program is a student loan forgiveness program that is specifically designed for teachers who work in low-income schools or in certain subject areas. The program is intended to encourage qualified teachers to work in these schools and subject areas by offering student loan forgiveness as an incentive.

To be eligible for the Teacher Loan Forgiveness Program, you must:

- Be a full-time, highly qualified teacher

- Have been teaching in a low-income school or in a subject area that is designated as a high-need field

- Have an outstanding balance on your Direct Loans or Stafford Loans

- Have been teaching for at least five consecutive years

- you may be eligible for forgiveness of up to $17,500.

If you meet these eligibility requirements and you are interested in applying for the Teacher Loan Forgiveness Program, you should visit the Federal Student Aid website to learn more and to submit an application. The amount of student loan forgiveness you can receive under this program depends on the specific terms of the program and the amount of your student loan debt.

USDA Veterinary Medicine Loan Repayment Program

The USDA Veterinary Medicine Loan Repayment Program (VMLRP) is a federally funded program that aims to recruit and retain veterinarians in underserved areas of the United States. The program pays up to $25,000 per year of a veterinarian’s qualified educational loans in exchange for a three-year commitment to serve in a designated shortage area.

To be eligible for the VMLRP, veterinarians must:

- Be a U.S. citizen or permanent resident

- Have received a Doctor of Veterinary Medicine (DVM) degree from an accredited college of veterinary medicine

- Have a valid veterinary license to practice in the United States

- Be willing to work in a designated shortage area for a period of three years

Veterinarians who are interested in participating in the VMLRP can apply through the USDA website. The application period for the program typically opens in the fall and closes in the winter.

U.S. Military Student Loan Forgiveness Options

There are several student loan forgiveness options available to military personnel in the United States:

- Public Service Loan Forgiveness (PSLF): This program forgives the remaining balance on Direct Loans for borrowers who have made 120 qualifying payments while working full-time for a government or non-profit organization.

- Military Loan Repayment Programs: Each branch of the military (Army, Navy, Air Force, etc.) offers loan repayment assistance to certain members who agree to enlist or re-enlist for a specific period of time.

- The Marine Gunnery Sergeant John David Fry Scholarship: This scholarship provides education benefits to the surviving spouse and children of a service member who died in the line of duty after September 10, 2001.

- The Department of Defense (DOD) Student Loan Repayment Program: This program provides student loan repayment assistance to eligible DOD employees in certain high-demand occupations.

- The National Guard Student Loan Repayment Program: This program offers student loan repayment assistance to members of the National Guard who agree to enlist or re-enlist for a specific period of time.

It’s worth noting that these programs have specific eligibility requirements and may have limits on the amount of student loan debt that can be forgiven. Military personnel interested in student loan forgiveness should check with their branch of service or the Department of Education to learn more about their options.

Air Force College Loan Repayment Program

The Air Force College Loan Repayment Program (CLRP) is a military benefit that helps eligible Air Force members repay their student loans. Under the program, the Air Force will repay a portion of an eligible member’s student loans in exchange for an enlistment or re-enlistment in the Air Force.

To be eligible for the Air Force CLRP, an individual must:

- Be a U.S. citizen

- Have a high school diploma or equivalent

- Have a qualifying score on the Armed Services Vocational Aptitude Battery (ASVAB) test

- Have a student loan or loans that are in repayment status

- Meet the Air Force’s physical and moral standards

The amount of student loan repayment an individual may receive through the Air Force CLRP depends on a variety of factors, including their military occupation, length of enlistment, and student loan balance. Interested individuals should speak with a recruiter for more information on the specific terms and conditions of the program.

Army College Loan Repayment Program

The Army College Loan Repayment Program (CLRP) is a military benefit that helps eligible Army members repay their student loans. Under the program, the Army will repay a portion of an eligible member’s student loans in exchange for enlistment or re-enlistment in the Army.The Army College Loan Repayment program offers significant student loan forgiveness to qualified individuals who enlist in certain critical military occupational specialties (MOS). Up to $65,000 of student loan debt can be forgiven through this program. However, it is important to note that this benefit must be included in the enlistment contract and comes at the cost of the Post 9/11 GI Bill, which may not be suitable for those planning on returning to college.

To be eligible for the Army CLRP, an individual must:

- Be a U.S. citizen

- Have a high school diploma or equivalent

- Have a qualifying score on the Armed Services Vocational Aptitude Battery (ASVAB) test

- Have a student loan or loans that are in repayment status

- Meet the Army’s physical and moral standards

The amount of student loan repayment an individual may receive through the Army CLRP depends on a variety of factors, including their military occupation, length of enlistment, and student loan balance. Interested individuals should speak with a recruiter for more information on the specific terms and conditions of the program.

National Guard Student Loan Repayment Program

The National Guard Student Loan Repayment Program is a military benefit that helps eligible National Guard members repay their student loans. Under the program, the National Guard will repay a portion of an eligible member’s student loans in exchange for an enlistment or re-enlistment in the National Guard.The National Guard Student Loan Repayment program provides loan forgiveness of up to $50,000 for qualifying Federal loans to guardsmen who enlist for a minimum of 6 years.

To be eligible for the National Guard Student Loan Repayment Program, an individual must:

- Be a member of the National Guard

- Have a student loan or loans that are in repayment status

- Meet the National Guard’s physical and moral standards

The amount of student loan repayment an individual may receive through the National Guard Student Loan Repayment Program depends on a variety of factors, including their military occupation, length of enlistment, and student loan balance. Interested individuals should speak with a recruiter for more information on the specific terms and conditions of the program.

Navy Student Loan Repayment Program

The Navy Student Loan Repayment Program is a benefit that pays off federally guaranteed student loans (up to $65,000) through three annual payments during a sailor’s first three years of service. To qualify for this program, you must enroll in it at the time of enlistment and have it included in your recruiting paperwork. This program is one of several education incentive programs offered by the Navy to help recruit and retain sailors.

State-Based Student Loan Forgiveness Options

Most states in the United States offer student loan forgiveness or repayment assistance programs to their residents. Some states have numerous options available.

Below is a list of the number of student loan forgiveness programs available in each state:

- Alabama: 0

- Alaska: 1

- Arizona: 3

- Arkansas: 2

- California: 3

- Colorado: 3

- Connecticut: 0

- Delaware: 1

- Florida: 2

- Georgia: 1

- Hawaii: 1

- Idaho: 1

- Illinois: 4

- Indiana: 1

- Iowa: 6

- Kansas: 3

- Kentucky: 1

- Louisiana: 3

- Maine: 5

- Maryland: 3

- Massachusetts: 1

- Michigan: 2

- Minnesota: 10

- Mississippi: 1

- Missouri: 3

- Montana: 3

- Nebraska: 1

- Nevada: 1

- New Hampshire: 2

- New Jersey: 3

- New Mexico: 3

- New York: 9

- North Carolina: 3

- North Dakota: 0

- Ohio: 2

- Oklahoma: 3

- Oregon: 3

- Pennsylvania: 2

- Rhode Island: 3

- South Carolina: 1

- South Dakota: 1

- Tennessee: 0

- Texas: 9

- Utah: 0

- Vermont: 5

- Virginia: 3

- Washington: 1

- West Virginia: 0

- Wisconsin: 1

- Wyoming: 2

- District of Columbia: 2

AmeriCorps Education Award

AmeriCorps is a national service program that offers individuals the opportunity to serve their community while also receiving education benefits. The AmeriCorps Education Award is a benefit provided to AmeriCorps members in recognition of their service. It is a financial aid award that can be used to pay for college, graduate school, or vocational training, or to pay off student loans.

To be eligible for the AmeriCorps Education Award, an individual must:

- Be at least 17 years old

- Be a U.S. citizen, U.S. national, or permanent resident

- Complete a term of service with AmeriCorps

The amount of the AmeriCorps Education Award is based on the length of the AmeriCorps service term. Members who complete a full-time service term of at least 1,700 hours can receive an award of up to $6,195. Members who complete a part-time service term of at least 900 hours can receive an award of up to $3,097.50. The award can be used to pay for education expenses such as tuition, fees, and books, or to pay off student loans.

The AmeriCorps Education Award is a valuable benefit that can help individuals further their education and reduce their student loan debt. Interested individuals can learn more about AmeriCorps and the Education Award by visiting the AmeriCorps website.

False Certification (Identity Theft) Discharge

If your student loans were taken out in your name due to identity theft or false certification (e.g., someone forged your signature or information on the loan), you may be eligible to have your loans discharged. This means that you would no longer be required to pay back the loans. If you believe you may be eligible for a loan discharge due to identity theft or false certification, you should contact your loan servicer or the Department of Education to learn more about the process.

Total and Permanent Disability Discharge

If you are permanently and totally disabled, you may be eligible to have your student loans discharged. To qualify, you must provide certification from a physician stating that you are unable to engage in substantial gainful activity due to a physical or mental impairment that is expected to result in death or that has already lasted for a continuous period of at least 60 months. If you are approved, any remaining balance on your Federal student loans will be discharged from the date that your physician certifies your application.

Alternatively, you may be eligible for loan discharge if you are certified as disabled by the Department of Veterans Affairs (VA) due to a service-related injury. If the VA certifies your application, any Federal student loan amounts owed after the date of your injury will be discharged, and any payments you made after your injury will be refunded to you.

You may also be eligible for loan discharge if you are certified as disabled by the Social Security Administration (SSA) and your notice of award for Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) benefits indicates that your next scheduled disability review will be within 5 to 7 years. If you are approved under this provision, any remaining balance on your Federal student loans will be discharged. This benefit has recently become tax-free thanks to Trump’s student loan reform.

Bankruptcy Discharge

Contrary to popular belief, it is possible to discharge student loans in bankruptcy, although it is rare. To do so, you must prove to a judge that repaying your loans would create an undue hardship. This requires you to demonstrate that there is no likelihood that you will be able to repay the loans in the future. This can be difficult to prove because the future is uncertain, and it may be hard to predict whether you will be able to earn enough to repay the loans over the course of many years. As a result, it can be challenging to discharge Federal student loans through bankruptcy, but it is not impossible.

If you are considering pursuing this option, it is important to have a lawyer who is well-versed in the requirements for student loan discharge in bankruptcy. Unfortunately, many lawyers and even some judges may not be familiar with how to handle student loans in bankruptcy proceedings.

Perkins Loan Cancellation Options

Perkins loans are a type of Federal student loan that are offered and administered by the school you attend. These loans are typically awarded to high-need students who are attending or planning to attend college. To determine if you are eligible for a Perkins loan, it is important to complete the Free Application for Federal Student Aid (FAFSA) each year and check your financial aid award.

Perkins loans have unique requirements for loan cancellation based on the field in which you work. Depending on your profession (see list below), you may be able to have up to 100% of your Perkins loan cancelled over the course of 5 years (except when indicated). Specifically, you may be able to have 15% of your principal balance and accrued interest cancelled after your first and second year of qualifying service, 20% cancelled after your third and fourth year, and 30% cancelled after your fifth year.

Perkins loans also offer concurrent deferment, which means you can postpone repayment of your loan while you are performing qualifying service.

The professions eligible for cancellation and the requirements are listed below.

- Active-Duty Imminent Danger Area: If you serve in the U.S. Armed Forces in a hostile fire or imminent danger area, you may be eligible for student loan forgiveness. The amount you can receive depends on when your active duty ended. If it ended before August 14, 2008, you may receive forgiveness for up to 50% of your outstanding loans. If your active duty includes or began after that date, you may receive up to 100% forgiveness of your outstanding loans.

- Attorney: If you are a full-time attorney employed in a Federal or community defender organization and perform qualified service that began on or after August 14, 2008, you may be eligible for up to 100% student loan forgiveness.

- Child or Family Services Agency: If you are a full-time employee of a public or non-profit child or family services agency providing services to high-risk children and their families from low-income communities, you may be eligible for up to 100% student loan forgiveness.

- Firefighter Or Law Enforcement: If you are a full-time firefighter, law enforcement officer, or corrections officer and your service began on or after August 14, 2008, you may be eligible for up to 100% student loan forgiveness.

- HeadStart: If you are a full-time staff member in the education component of a HeadStart program, you may be eligible for up to 100% forgiveness of your loans, paid out as 15% of the principal balance and accrued interest for each year of service.

- Intervention Services Provider: If you are a full-time qualified professional provider of early intervention services for the disabled and your service began on or after August 14, 2008, you may be eligible for up to 100% student loan forgiveness.

- Librarian: If you are a librarian with a master’s degree working in a Title I-eligible elementary or secondary school or in a public library serving Title I-eligible schools (a list of qualifying schools can be found here) and you were employed on or after August 14, 2008, you may be eligible for up to 100% student loan forgiveness.

- Nurse or Medical Technician: If you are a full-time nurse or medical technician, you may be eligible for up to 100% student loan forgiveness. Our full guide to student loan forgiveness for nurses provides more information on this option.

- Pre-kindergarten or Child Care: If you are a full-time staff member in a pre-kindergarten or child care program that is licensed or regulated by a state and you were employed on or after August 14, 2008, you may be eligible for up to 100% student loan forgiveness.

- Speech Pathologist: If you are a full-time speech pathologist with a master’s degree working in a Title I-eligible elementary or secondary school, you may be eligible for up to 100% student loan forgiveness.

- Teacher – Shortage Area: If you are a full-time teacher of math, science, foreign languages, bilingual education, or other fields designated as teacher shortage areas, you may be eligible for up to 100% forgiveness of your loans.

- Teacher – Special Education: If you are a full-time special education teacher of children with disabilities in a public school, nonprofit elementary or secondary school, or educational service agency, you may be eligible for up to 100% student loan forgiveness. If your service is at an educational service agency, it must include August 14, 2008, or have begun on or after that date.

- Tribal College Faculty: If you are a full-time faculty member at a tribal college or university and your service includes August 14, 2008, or began on or after that date, you may be eligible for up to 100% student loan forgiveness.

Notice For Private Student Loan Debt

Unfortunately, there are no specific programs that offer student loan forgiveness for private loans. Private student loans behave more like car loans or mortgages, where you pay a fixed amount and do not have access to special programs. However, there are still some options available for those struggling with private student loan debt. One option is student loan refinancing, which can potentially lower your interest rate or change your repayment length, potentially reducing your monthly payment and saving you money. Credible is a website that allows you to compare refinancing options and see if it makes sense for you. College Investor readers can also receive a $1,000 gift card bonus when they refinance with Credible. For more information on options for managing private student loan debt, check out our guide on the topic.

Tax Consequences From Student Loan Forgiveness

It’s important to note that while these “secret” student loan forgiveness options may be helpful for some borrowers, they may also result in tax consequences. However, the American Recovery Act signed by President Biden makes all loan discharges and student loan forgiveness tax-free through December 31, 2025, regardless of loan type or program. Keep in mind that state taxes may still apply.

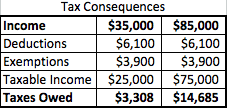

Previously, the forgiven amount of a student loan was added to the borrower’s taxable income for the year. For example, if a borrower had $50,000 in student loans forgiven, this amount would be considered income and added to the borrower’s total income for the year. This could lead to a higher tax bill. However, for many borrowers, this tax bill may be more manageable than the original debt itself. The following table illustrates the potential tax consequences of student loan forgiveness:

Tax Consequences As shown in the table, using these repayment plans may result in an additional $11,377 in Federal Income Tax in the year of forgiveness. However, this amount may still be cheaper than paying the original $50,000 plus interest. Additionally, there are options to work out a repayment plan with the IRS if necessary.

Student Loan Forgiveness FAQs

- What is student loan forgiveness? Student loan forgiveness is a way to cancel all or part of your student loan debt. There are several programs available that may forgive your student loans if you meet certain requirements, such as working in a certain profession, serving in the military, or making a certain number of payments.

- How do I qualify for student loan forgiveness? Eligibility requirements for student loan forgiveness programs vary. Some programs may require you to work in a certain profession, such as teaching or public service, while others may require you to make a certain number of payments or serve in the military. Some programs may also have income or employment requirements.

- How much student loan debt can be forgiven? The amount of student loan debt that can be forgiven through these programs varies. Some programs may forgive all of your student loan debt, while others may forgive only a portion.

- Is student loan forgiveness tax-free? The American Recovery Act signed by President Biden makes all student loan forgiveness tax-free through December 31, 2025, regardless of loan type or program. However, state taxes may still apply. Previously, the forgiven amount of a student loan was added to the borrower’s taxable income for the year.

- What are the alternatives to student loan forgiveness? If you do not qualify for student loan forgiveness or prefer not to pursue it, there are other options to consider. These may include student loan consolidation, student loan refinancing, or income-driven repayment plans. These options can lower your monthly payments or help you pay off your student loans more quickly.

- Where can I get more information about student loan forgiveness? To learn more about student loan forgiveness and other options for managing your student loan debt, you can visit the Department of Education’s website or contact your loan servicer. You can also consider seeking advice from a financial professional or a student loan lawyer.